- An Insight into Vitality

Vitality stands out as a distinct life insurance provider within our assessments. The company distinguishes itself by placing significant importance on the correlation between life insurance and maintaining a healthy lifestyle, evident through its shared-value insurance approach. The Vitality Programme offers policyholders incentives and discounts for adopting healthy lifestyle choices.

In collaboration with numerous local sports teams and organizations, Vitality has fostered partnerships, such as with Parkrun, encouraging nearly three million Britons to engage in weekly 5km runs. Officially introduced to the United Kingdom market in 2004, Vitality operates globally in 30 countries and is wholly owned by South African firm Discovery.

Benefits:

- Discounts available for gym memberships and wearable technology, encouraging lifestyle improvements.

- Offers an optional Optimiser add-on, monitoring activity levels and potentially reducing premiums by up to 40%.

- Provides the option to include cover for a tax-free payout in the event of a serious illness affecting you or your child.

- Many policies can be purchased directly without the need for an agent or adviser.

Drawbacks:

- Enrollment in the membership system might limit flexibility and hinder the ability to explore other insurance options.

- Consistent maintenance of a healthy lifestyle is necessary to qualify for discounts.

- Smokers are unlikely to receive any discount on premiums.

- Vitality Life Insurance Evaluation

Vitality’s philosophy centers on the correlation between a healthy lifestyle and reduced insurance claims. The company incentivizes its members to embrace healthier habits by providing rewards and discounts. Upon enrollment, all new members are automatically enrolled in Vitality Select rewards. Additionally, customers can choose to include the complimentary Optimiser plan, which expedites underwriting processes and reduces premiums based on their healthy lifestyle.

Distinct from conventional insurance terminology, Vitality often mentions a Personal Protection Plan, encompassing various life insurance offerings such as term and whole life policies. They utilize a tiered system – Bronze, Silver, Gold, and Platinum – determined by the accumulation of healthy lifestyle points. These points are earned through activities like using an activity tracker, undergoing a Vitality Healthcheck, attending wellness workshops, or exercising at the gym.

Vitality claims to offer premiums that are 30-40% lower than competitors, although these premiums may increase annually depending on one’s fitness, activity level, and health. For instance, Bronze-level members may experience a yearly premium increase of 2.5%, whereas Silver-level members could see a lower increase of 1.5% by advancing to the Silver tier. Gold-level premiums increase by 0.5%, while Platinum-level premiums remain unchanged. Sustaining a healthy status could result in paying 30% less over the policy’s term compared to purchasing from another insurer.

Coverage Options: Vitality provides term insurance, whole life, joint life, family life policies, and serious illness cover. While there’s no specific policy for individuals over 50, Vitality markets term and whole life policies to this demographic. Policyholders can select level, term, decreasing term, or index-linked plans to hedge against inflation. Additional options include serious illness, mortgage protection, and income protection.

Coverage Limits: The maximum sum assured is £7.2 million for indexed increasing plans and £18 million for level term plans. Requests to exceed these limits may be considered, subject to agreement with the reinsurance partner.

Coverage Restrictions: Term and whole life plans have a minimum term of five years, and fixed-term life cover extends until age 90. There are no maximum term limits for whole life cover. Remarkably, Vitality accepts applicants as young as 16 for term and whole life insurance. Children under 23 can also be included in an adult’s plan for child serious illness cover.

Vitality caters to individuals committed to a healthy lifestyle, offering rewards and discounts as incentives. It presents a comprehensive range of coverage options, including term and whole life policies, accompanied by numerous perks. However, if you don’t currently lead an active lifestyle or have no plans to do so, Vitality might not be the ideal life insurance provider for you.

- What Types of Life Insurance Policies Does Vitality Provide?

Vitality presents a range of life insurance options, including both term and whole life coverage, each with various payout structures such as level, decreasing, or index-linked. Additionally, there are several supplementary features and customization choices available to tailor your protection plan to your specific needs.

- Term Life Insurance

Under term life insurance, a lump sum is provided to your family in the event of your death or diagnosis of a terminal illness during the specified coverage period (the term).

- Term Life – Level:

With this option, you determine the lump sum your family will receive if you pass away at the outset of the policy. This amount remains constant throughout the term unless you opt to modify it. Your family will receive this fixed sum as a lump sum payment.

- Term Life – Decreasing:

Decreasing term coverage is typically aligned with decreasing financial obligations, such as mortgage repayments. As you gradually pay off your mortgage, the outstanding debt decreases, consequently reducing the amount your family would need to settle it. As a result, premiums for decreasing term policies are generally lower compared to level term policies.

- Term Life – Increasing:

Vitality offers an index-linked payout option that increases annually in accordance with the Retail Prices Index (RPI), with a maximum annual increase of 10%. This choice is suitable for individuals concerned about inflation eroding the value of their payout over time. Typically, this option entails higher premiums compared to level or decreasing term insurance.

- Whole of Life Insurance

Unlike term life policies, which have a predetermined coverage period, whole of life insurance provides a lump sum payout upon your death with no maximum age limit. However, this type of insurance tends to be more expensive. Notably, Vitality is unique in offering whole of life insurance directly without the need for an intermediary, such as an agent or financial adviser.

Vitality provides whole of life coverage with options for level, decreasing, or increasing (indexed) payouts. Additionally, policyholders can opt for LifestyleCare Cover, allowing access to a portion or all of the lump sum in the event they are unable to care for themselves.

Although Vitality doesn’t offer a dedicated over 50s policy, it extends term and whole of life insurance options to individuals in that age bracket.

- Exploring Additional Coverage Options with Vitality

Vitality provides a range of additional cover options tailored to individual needs, including income protection, coverage for serious illnesses, protection for children, premium waivers, and various other choices. The company encourages the development of personalized protection plans that promote healthy habits. Additionally, by participating in their advanced health and lifestyle program, members can unlock even more benefits and rewards.

Serious illness cover is available with three levels of coverage, each encompassing an increasing number of conditions. Opting for higher plans may entitle policyholders to payouts of up to three times their cover amount.

- Understanding the Cost of Life Insurance with Vitality

While Vitality doesn’t disclose standard prices on its website, obtaining an online quote is straightforward through a brief survey. The premium for life insurance with Vitality is determined by several factors, including age, occupation, medical history, and overall health and lifestyle choices (such as smoking habits). Discounts are applied based on improvements in health and fitness over the enrollment period. Policyholders who achieve higher levels of fitness and health can benefit from substantial discounts and fixed premiums, whereas those with less active lifestyles may experience annual increases in premiums.

- Is Vitality Life insurance worth it? – an unbiased view

Vitality’s distinct pink branding and innovative insurance approach have garnered attention from both the public and the industry. However, the question arises: Is Vitality life insurance truly worthwhile? While the eye-catching discounts and perks, such as up to 50% off gym memberships and complimentary Apple watches, may seem enticing, it’s essential to delve deeper into the insurance products themselves.

To make an informed decision, consulting an independent expert is advisable. They can provide insights into various options, offer quotes, and discuss alternatives before committing. Additionally, purchasers are entitled to receive up to £100 cashback upon buying insurance, regardless of whether they choose Vitality or not.

In this analysis, we aim to go beyond the surface benefits and examine Vitality’s life insurance offerings comprehensively. We explore what Vitality provides its customers, how its life insurance compares to other market alternatives, the nuances of its critical illness insurance, and the suitability of Vitality life insurance for different individuals.

Vitality’s life insurance suite encompasses familiar products like life insurance, income protection insurance, and whole of life insurance. Notably, their life insurance includes terminal illness benefit as standard, allowing for an early claim if the policyholder is diagnosed with a life expectancy of less than 12 months—a feature commonly found in reputable life insurance policies.

One unique aspect of Vitality’s offerings is their version of critical illness insurance, termed Serious Illness Cover. Introduced in 2007, this flagship product sets Vitality apart in the UK insurance market. We’ll delve into the specifics of Serious Illness Cover shortly.

Both Vitality’s life insurance and Serious Illness Cover boast a 5-star Defaqto rating, positioning them among the most comprehensive policies available. This rating underscores their extensive coverage and quality within the insurance landscape.

- Vitality offers a range of life insurance options tailored to individual needs:

Term Life Insurance: This policy provides a payout if any of the insured individuals pass away within the specified term. The coverage period determines how long the insurance remains in effect. The amount of coverage can remain constant throughout the term (known as level term assurance), decrease gradually over time (known as decreasing life assurance), or remain steady but paid out periodically instead of as a lump sum (known as family income benefit).

Whole of Life Insurance: This policy has no set term, providing coverage until the insured individual’s death. Due to its lifelong coverage, this option tends to be more expensive than term life insurance.

Income Protection: This policy pays a regular income, which is a percentage of your salary, if you’re unable to work due to injury or illness.

In addition to these core options, Vitality offers supplementary coverage:

Serious Illness Cover: This insurance pays a lump sum if you’re diagnosed with a serious illness. The payout amount varies based on the severity of the illness and the chosen coverage level (1x, 2x, or 3x).

Dementia and Frail Care Cover: Available exclusively with serious illness insurance, this option allows policyholders to utilize any remaining cover for later life protection. If diagnosed with conditions like Alzheimer’s, Dementia, or requiring long-term care, the benefit pays out to assist with activities of daily living requiring carer assistance.

- What is Vitality Serious Illness Insurance cover?

Vitality Serious Illness Insurance cover is the counterpart of traditional critical illness insurance offered by Vitality. To grasp its distinctions from conventional critical illness insurance, it’s essential to revisit the fundamentals of critical illness coverage.

Critical illness insurance originated in the 1980s under the name “dread disease insurance.” This type of insurance provided a payout if the policyholder was diagnosed with specific critical illnesses, such as cancer. The payout could be utilized at the policyholder’s discretion, often to settle mortgages or other financial obligations, and the policy would subsequently terminate.

During the 1980s, the prognosis for individuals diagnosed with illnesses like cancer was grimmer compared to today. Due to limited screening techniques and less effective treatments, survival rates were lower, necessitating a lump-sum payout to alleviate potential financial burdens during recovery or to manage affairs in the event of terminal illness.

Although the conditions covered may vary, modern critical illness policies typically operate on similar principles, offering a lump-sum payment upon diagnosis of a covered illness or in the event of death. Consequently, these policies tend to be costly.

- What sets Vitality Serious Illness cover apart?

Vitality’s approach to critical illness insurance distinguishes itself from traditional models in two significant ways:

- Tailored Payouts: Rather than providing a lump-sum payout equal to the full coverage amount, Vitality Serious Illness insurance adjusts payouts based on the severity of the diagnosed illness. For instance, a Stage I cancer diagnosis might yield 25% of the coverage amount, while a Stage IV diagnosis could result in 100% coverage. This approach acknowledges the reduced financial impact of illnesses today, thanks to advancements in treatment methods.

- Multi-Claim Capability: Unlike most critical illness policies, which typically pay out once and then expire, Vitality allows policyholders to make multiple claims. Recognizing the increase in life expectancy and the improved outcomes of once life-threatening illnesses, Vitality believes policies should adapt to reflect this reality, enabling multiple payouts.

- Vitality’s Tiered Serious Illness Cover Explained:

Vitality offers three tiers of serious illness cover, each with distinct features:

- Serious Illness Cover 1x: This standard product covers 114 conditions based on severity and allows for multiple payouts until the coverage amount is exhausted.

- Serious Illness Cover 2x: Providing coverage for an additional 29 conditions, totaling 143, with full payouts for 74 conditions. It allows for up to two payouts based on the chosen coverage level.

- Serious Illness Cover 3x: Vitality’s premier offering includes all the benefits of 2x, plus coverage for an additional 31 lower-severity conditions, totaling 174. It enables up to three payouts over the policy’s duration, based on the chosen coverage level.

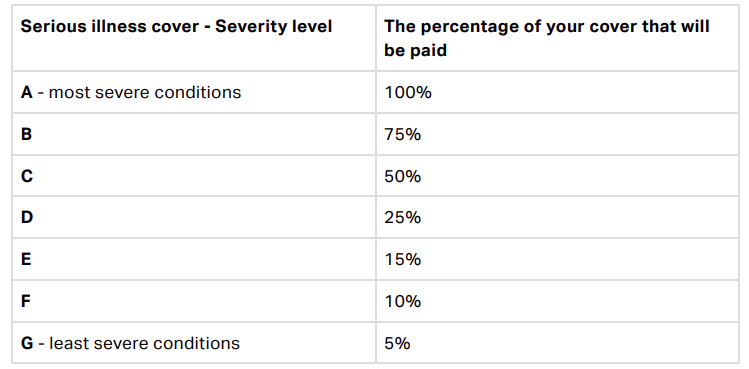

The percentage of the coverage amount disbursed upon diagnosis depends on the severity band in which the illness falls. Vitality categorizes conditions into seven bands, ranging from A (most severe, warranting 100% payout) to G (least severe, resulting in a 5% payout).