You’re likely aware that renters insurance is designed to protect tenants, while homeowners insurance is tailored to safeguard homeowners and their properties. If you’ve started exploring renters insurance options, you may have noticed that it can often be quite affordable. Conversely, delving into homeowners insurance for the first time may reveal that its cost tends to be higher compared to renters insurance. This discrepancy is due to the fact that homeowners insurance not only covers the structure of your home but typically offers more extensive coverage overall compared to renters insurance.

- Renters insurance vs. homeowners insurance cost

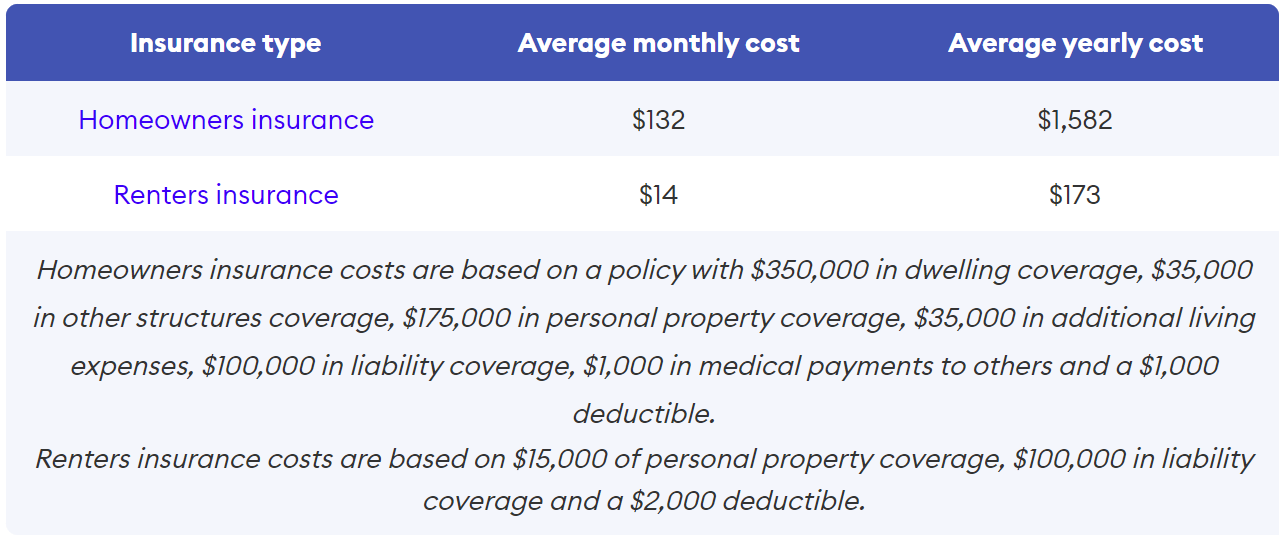

In terms of cost, renters insurance is generally considered inexpensive. However, the actual price of your policy will depend on various factors such as your state of residence, the type of dwelling you live in, your credit score, and the coverage limits you choose.

On the other hand, homeowners insurance typically comes at a higher cost than renters insurance. Similar to renters insurance, several factors influence the price of your homeowners policy, including your location, the type of home you own, the construction of your home’s roof, any past insurance claims you’ve made, and the specific coverage options you select.

- What’s the difference between renters and homeowners insurance?

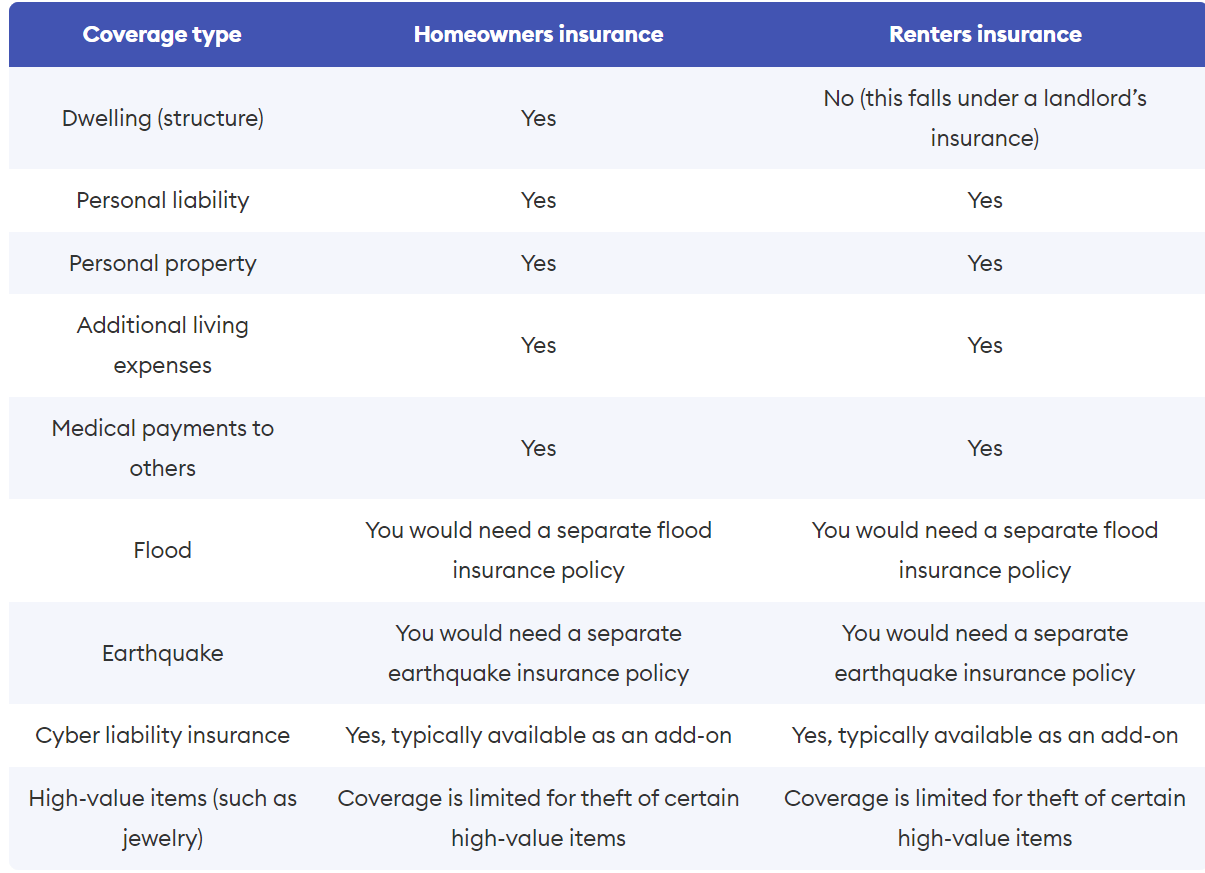

What sets renters insurance apart from homeowners insurance? The most notable difference lies in their coverage of the physical structure. While homeowners insurance shields the physical structure of the home against covered risks, renters insurance does not extend to the building occupied by the tenant. Homeowners policies typically include dwelling coverage, which may cover the costs of repairing or rebuilding the home after damage from a covered peril. Conversely, renters policies typically lack dwelling coverage. In the event of damage to an apartment building or rental house due to a covered peril, it’s the responsibility of the building owner or homeowner to have insurance on the structure.

Both renters and homeowners policies provide personal property coverage to safeguard belongings, but the determination of coverage limits differs. Renters insurance policyholders usually have the flexibility to set their own limit based on the value of their possessions. For homeowners policies, personal property coverage is often calculated as a percentage of the dwelling coverage limit.

Loss of use coverage is another feature present in both renters and homeowners policies, although the coverage limits may vary. Homeowners policies typically offer 10% or 20% of the dwelling coverage amount for loss of use coverage. In contrast, renters policies may have a loss of use coverage limit set as a flat amount ranging from $3,000 to $5,000, or it may be a percentage of the personal property coverage limit, depending on the insurer.

While neither homeowners nor renters insurance is legally mandated by state law, homeowners insurance is typically required by lenders if there is a mortgage on the property. On the other hand, rental companies or landlords may require renters insurance before a tenant can occupy an apartment unit or rental house.

- Comparison of Homeowners Insurance and Renters Insurance

When deciding between homeowners insurance and renters insurance, several factors should be considered:

- Who Needs Coverage?

- Homeowners insurance is essential for those who own their homes, often being a requirement if a mortgage is in place.

- Renters insurance is necessary for tenants, with many landlords mandating its purchase.

- Coverage Details:

- Homeowners insurance typically covers the dwelling itself, other structures on the property, accidental property damage, and liability for injuries to others. Additionally, it may include coverage for additional living expenses during temporary displacement.

- Renters insurance primarily covers personal belongings, accidental property damage, liability for injuries to others, and may also include coverage for temporary living expenses due to covered events.

- Available Discounts:

- Homeowners insurance policies may offer discounts for safety and security features, the age of the roof, or by bundling with other insurance policies like auto insurance.

- Renters insurance providers also offer discounts, often for bundling with auto insurance, maintaining home safety features, or opting for paperless billing.

- Payment Methods:

- Premiums for both homeowners and renters insurance can typically be paid online, through electronic fund transfer (EFT), or by mailing a check to the insurer. Some homeowners may pay premiums through an escrow account.

- Payment frequency usually includes options for monthly, quarterly, semi-annual, or annual payments.

- Deductibles:

- Both types of insurance policies involve deductibles for claims related to theft and property damage, while liability claims typically don’t have deductibles.

- Deductible amounts commonly range from $500 to $1,000, meaning that if a claim is filed for damaged or stolen property, the deductible amount is subtracted from the claims check issued by the insurer. For instance, if a burst pipe damages furniture and the deductible is $500, that amount is deducted from the reimbursement check.

- Understanding the Contrasts Between Renters Insurance and Home Insurance Coverage

When comparing renters insurance to homeowners insurance, a notable distinction lies in what each policy covers. Homeowners insurance typically extends coverage to structures such as the house itself, fences, sheds, and other related structures. In contrast, renters insurance does not include coverage for these structures, as the landlord’s insurance typically handles damages to the building.

For instance, if a fire occurs and damages a house owned by the insured, homeowners insurance would facilitate the repairs to the building. Conversely, if a rented apartment experiences fire damage, the repairs to the building would typically fall under the landlord’s insurance policy.

- Evaluating the Coverage of Homeowners Insurance versus Renters Insurance

Both homeowners and renters insurance policies provide coverage for various risks, often referred to as “perils.” These perils encompass a range of potential problems that may occur. For instance, a homeowners insurance policy typically covers damages caused by fire to the house and personal belongings within it.

Personal property coverage under both homeowners and renters insurance usually extends to 16 perils, which include:

- Accidental discharge or overflow of water or steam

- Damage from aircraft, including spacecraft and self-propelled vehicles

- Civil commotion or riot-related damages

- Explosions

- Damages caused by falling objects

- Freezing-related damages

- Hail or windstorm damages

- Vandalism or malicious mischief

- Damages from lightning or fire

- Smoke-related damages

- Sudden and accidental damage from electrical currents

- Structural damages from tearing apart, cracking, burning, or bulging

- Theft

- Damages caused by vehicles

- Weight of ice, sleet, or snow

- Damages resulting from volcanic eruptions

The most common homeowners insurance policy is the HO-3, which operates on an “open-perils” basis for the house itself. This means it covers damages from any cause except for those explicitly listed as exclusions. Common exclusions may include power failure, floods, earthquakes, negligence, normal wear and tear, damages caused by pets or insects, and negligence.

However, while an HO-3 policy typically covers personal possessions for 16 specified perils, homeowners can opt for an HO-5 policy for more comprehensive coverage. The HO-5 policy offers protection against all perils except those explicitly excluded (like floods), and it includes replacement cost coverage for damaged or stolen items, rather than offering actual cash value coverage. In contrast, homeowners with an HO-3 policy may need to add an endorsement for replacement cost coverage.

- Key Coverage Features in Homeowners and Renters Insurance

Both homeowners and renters insurance encompass various types of coverage to protect your belongings and liability.

Protection for Personal Property

- This coverage caters to the repair or replacement of your belongings, ranging from furniture, electronics, and clothing to sports equipment and tools. Typically, your possessions are covered wherever you take them, be it in your car or during vacations. However, coverage for high-value items like jewelry might be capped (e.g., $1,500). For comprehensive coverage of valuable items, scheduling personal property ensures separate insurance with full coverage against theft and damage.

Personal Liability Safeguard

- In the event of accidental injuries or property damage to others, personal liability coverage steps in to cover medical expenses, property damage costs, and legal fees. For instance, if your dog injures someone at a park, your liability insurance can assist with their medical bills. Should you require additional liability coverage beyond your home or renters insurance, exploring an umbrella insurance policy is advisable.

Assistance with Additional Living Expenses

- Additional living expenses (ALE) coverage supports temporary housing and related expenses if circumstances covered by your policy, such as a fire, render your home uninhabitable. This includes expenses like hotel accommodation, takeout meals, and services such as pet boarding and laundry.

Medical Payments Reimbursement

- Medical payments coverage reimburses minor medical expenses for a guest injured in your home or apartment, irrespective of fault. This provision facilitates prompt settlement of small medical bills. Moreover, it extends coverage to minor medical expenses resulting from incidents away from your residence, such as your dog biting someone in a park. Typically available in modest amounts, such as $1,000 to $5,000, this coverage offers a safety net for unexpected medical costs.

- Homeowners vs. Renters Insurance: What Does it Cost?

- Why Homeowners Insurance Costs More Than Renters Insurance

The price disparity between homeowners insurance and renters insurance largely stems from the coverage scope. Homeowners insurance is pricier due to its comprehensive protection, which includes rebuilding costs in case of events like fires that damage the house. In contrast, renters insurance primarily covers personal belongings; structural repairs are typically the responsibility of the landlord’s insurance policy.

Furthermore, homeowners insurance extends coverage to auxiliary structures such as decks, detached garages, or fences, whereas renters insurance solely focuses on personal possessions, leaving structural concerns to the landlord’s coverage.

- Determining Renters Insurance Needs

Assessing your renters insurance needs begins with compiling a home inventory. This inventory provides insights into the required personal property coverage, safeguarding belongings against perils like tornadoes or fires.

Creating a home inventory can be a straightforward process, whether through manual documentation or utilizing digital tools like smartphone apps such as the one offered by the National Association of Insurance Commissioners. Details such as item descriptions, estimated values, serial numbers, and receipts, if available, should be recorded.

However, personal property coverage is just one facet. It’s crucial not to underestimate the importance of acquiring adequate liability coverage, particularly for individuals with substantial assets. While a standard renters policy might offer a base liability protection of $100,000, this might be insufficient for many. It’s essential to ensure that your liability coverage adequately protects against potential losses in legal disputes.

Additionally, determining the appropriate coverage for additional living expenses is vital. Insurance companies may offer a fixed amount for such coverage, or it may be calculated as a percentage of your personal property coverage. Should more extensive coverage be necessary, it’s typically available for purchase.

- Navigating Homeowners or Renters Insurance

Whether you’re in the market for homeowners or renters insurance, the process of securing coverage shares similarities. Here are some guiding tips to assist you in finding the appropriate policy.

How to Secure Homeowners Insurance

Acquiring homeowners insurance is a crucial step in homeownership, yet the process is relatively straightforward. Here’s a step-by-step guide on how to obtain homeowners insurance:

- Assess your homeowners insurance needs based on factors such as the size, age, and construction materials of your home.

- Compile essential information about your property, including its construction year, room count, square footage, and building materials.

- Obtain and compare homeowners insurance quotes from various insurers to ensure you find the best coverage at a competitive rate.

- Consider that insurance premiums for homeownership can vary significantly depending on factors such as geographical location, property age, and the estimated cost of rebuilding your home.

How to Secure Renters Insurance

Securing a renters insurance policy follows a similar trajectory to that of homeowners insurance. Here’s a rundown of how to obtain renters insurance:

- Determine the extent of personal property coverage you require by conducting a thorough inventory of your belongings.

- Evaluate the amount of liability insurance needed based on your financial standing and assets.

- Compare renters insurance quotes from multiple insurers to find the most suitable coverage for your needs.

- Keep in mind that renters insurance premiums are influenced by factors such as location and desired coverage limits.

Renters Insurance vs. Landlord Insurance: Understanding the Differences

It’s important to note that renters insurance and landlord insurance serve distinct purposes:

- Renters insurance safeguards your personal belongings against perils like theft and fire. Additionally, it provides liability coverage for accidental injuries and property damage to others. Furthermore, it may cover additional living expenses if your residence becomes uninhabitable due to a covered incident.

- On the other hand, landlord insurance primarily protects the building and other structures from risks such as fires, storms, and vandalism. It does not extend coverage to tenants’ personal belongings.