Comparing Medicare and Private Insurance

Medicare is often preferred by eligible individuals seeking affordable rates, while private health insurance offers greater flexibility.

Medicare is a government-administered health insurance program, while private health insurance is directly provided by insurance companies.

However, the origin of coverage doesn’t determine its privacy. Certain Medicare benefits are offered by private insurers, and individuals can also have both types of coverage simultaneously.

Medicare is federally provided health insurance coverage

a, Medicare

Medicare, a federally administered health insurance program, extends coverage to individuals aged 65 and above, with eligibility also open to those with qualifying disabilities who are younger. The coverage comprises four main parts:

- Part A: Also known as hospital insurance, Medicare Part A caters to expenses related to inpatient care in hospitals, nursing facilities, hospices, and similar settings. Part A is integral to Original Medicare and is overseen by the federal government. Additionally, individuals may opt for a Medicare Supplement policy, commonly referred to as a Medigap policy, which supplements Original Medicare Parts A and B, thereby potentially reducing out-of-pocket expenses.

- Part B of Original Medicare covers expenses related to doctor visits and outpatient services. It is administered by the government, serving as a crucial component in providing healthcare coverage for beneficiaries.

- Medicare Part C, commonly known as Medicare Advantage, consolidates various components of Medicare into a single plan. Private insurance companies market Medicare Advantage plans under government authorization.

- Medicare Part D provides coverage for prescription drugs and can be obtained either as a separate policy in addition to Parts A and B, or it can be included within a Medicare Advantage plan. Similar to Part C, Part D is offered by private insurance companies.

b, Private health insurance

Private health insurance encompasses coverage obtained either through an employer or purchased independently. Employer-provided coverage, known as group insurance, is one option. Alternatively, individuals can procure private health insurance directly from an insurance provider or through a marketplace platform. Individual health insurance becomes relevant for those without employer-sponsored coverage or Medicare eligibility. Unlike government-sponsored plans, private health insurance typically offers a wider array of coverage options, albeit at a higher cost.

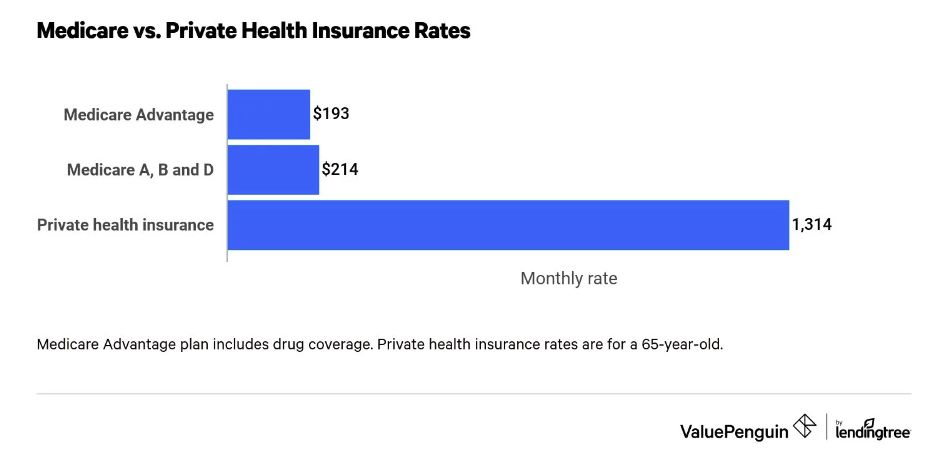

Medicare vs. private health insurance: Rates

Comparing Medicare with private health insurance, the latter tends to be more expensive, although costs vary depending on selected coverage. Medicare expenses hinge on the chosen plan structure. For instance, a Medicare Advantage plan inclusive of drug coverage averages around $192.90 monthly, whereas purchasing Parts A, B, and D separately tallies up to an average of $213.90 per month. Private health insurance, on the other hand, presents an average monthly cost of $1,314.00 for a 65-year-old enrolled in a Silver plan. This figure fluctuates based on factors such as age, location, tobacco use, policyholder count, insurance company choice, and plan level. Individuals acquiring coverage through federal or state marketplaces may be eligible for income-based premium tax credits, potentially reducing premiums. Moreover, employer-sponsored group insurance often involves the employer subsidizing a portion of the cost.

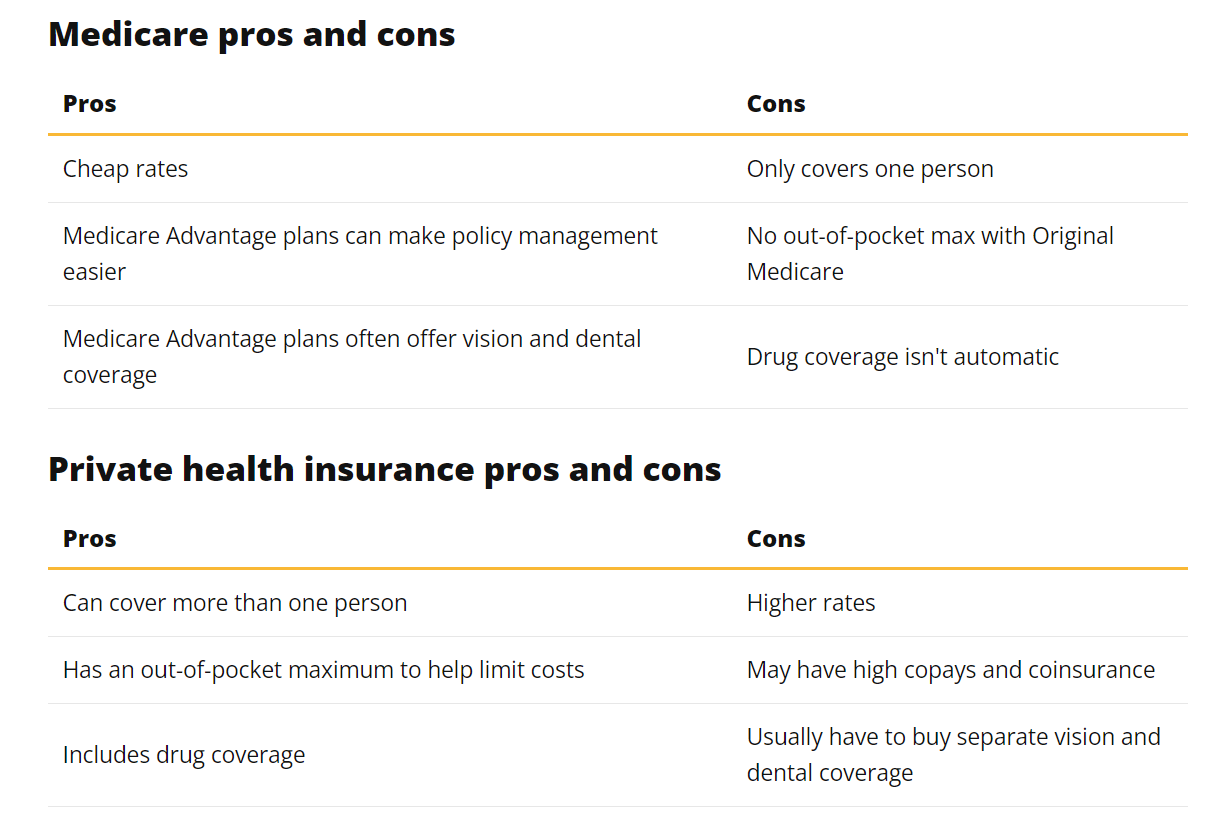

Pros and cons of private health insurance and Medicare

Medicare offers solid coverage for eligible individuals, yet private health insurance might be preferable if you’re looking to include additional individuals under your policy due to its flexibility and customization options.

Can you have private insurance and Medicare?

Yes, it’s possible to have both private health insurance and Medicare simultaneously.

If you’re enrolled in both Medicare and a private health insurance plan, such as a group or individual plan, the coordination of benefits rules come into play. This means that Medicare will coordinate with your private insurer to determine which plan will pay first for your medical expenses. For instance, if you’re 65 or older and covered by a group plan from an employer with more than 20 employees, your employer-sponsored insurance will generally be the primary payer, and Medicare will be secondary.

If you have an individual plan from the federal or state marketplace when you become eligible for Medicare, you can maintain both plans. However, you will lose any premium tax credits you were receiving for your marketplace plan. It’s important to note that it’s illegal for someone to knowingly sell you a marketplace plan if you’re already enrolled in Medicare.

Frequently asked questions:

Is private insurance better than Medicare?

- Private insurance isn’t inherently better than Medicare; it simply offers different benefits. While private health insurance tends to be more expensive than Medicare, it may provide more flexibility, particularly if you want to include a spouse or dependent children on your policy. Medicare, on the other hand, may be a preferable option if cost is your primary concern and you qualify for it.

Is Medicare good insurance?

- Medicare can be effective insurance, especially if you prioritize low-cost coverage. However, it doesn’t allow for the inclusion of spouses or dependent children on the policy, unlike private coverage. Therefore, if you need to extend coverage to other family members, Medicare may not be the most suitable choice for you.

Can I have Medicare and employer coverage simultaneously?

- Yes, it’s possible to have both Medicare and health insurance through your employer concurrently. Typically, your employer-sponsored plan will act as the primary insurer, with Medicare serving as secondary. However, there are situations where Medicare may be the primary payer, such as when the employer has fewer than 20 employees. In some cases, neither coverage may apply, such as when seeking care outside of the employer plan’s network.

Methodology

Data regarding Medicare costs were sourced from Medicare.gov and the Centers for Medicare & Medicaid Services (CMS). The analysis was based on average 2023 rates for Medicare Advantage plans, encompassing prescription drug coverage. Excluded from the study were special needs plans, Part-B-only plans, sanctioned plans, PACE plans, prepayment plans (HCPPs), Medicare savings account (MSA) plans, Medicare-Medicaid plans, and employer-sponsored plans. The average cost of Medicare Part D was derived from stand-alone prescription drug plans, excluding employer-sponsored and sanctioned plans.

The average cost of health insurance was gathered from public use files (PUFs) on the Centers for Medicare & Medicaid Services (CMS) government website, along with state-run marketplaces for states not utilizing the federal marketplace. Our analysis included plans and providers with county-level data available in the CMS Crosswalk file. Plans and providers not represented in this dataset were not included in our study. The average cost of health insurance was determined based on Silver plans for 65-year-olds, utilizing the age curve variations published by CMS.