Individuals seeking health insurance have two main options: Medicare or private companies. The decision on which option is optimal hinges on the individual’s healthcare requirements and financial circumstances.

Original Medicare is provided by the federal government, while private health insurance and Medicare Advantage plans are administered by private companies acting on behalf of the government.

The cost of private insurance varies depending on the type of plan and the extent of coverage. Some employers also offer private insurance as an employment benefit. It’s crucial for individuals to evaluate their healthcare needs to make informed decisions about their insurance plans.

To navigate through the process of selecting the most suitable insurance plan, understanding certain terms is essential:

- Deductible: This represents the annual amount that individuals must pay out of pocket within a specified timeframe before the insurer begins covering their medical expenses.

- Coinsurance: This refers to the percentage of treatment costs that individuals are responsible for covering themselves. For Medicare Part B, this typically amounts to 20%.

- Copayment: This denotes a fixed dollar amount that insured individuals are required to pay when receiving specific treatments. In the case of Medicare, copayments often apply to prescription drugs.

Coverage that private companies offer

Private companies offer a range of health insurance coverage options approved by Medicare, which may include:

- Help with Medicare expenses like deductibles, copayments, and coinsurance.

- Prescription drug coverage provided by Medicare Part D plans.

- Additional benefits such as vision, hearing, and dental care, often offered through Medicare Advantage plans that incorporate original Medicare (Part A and Part B) coverage.

To qualify for these private insurance plans, individuals must first be enrolled in original Medicare.

Who is eligible for Medicare?

Medicare eligibility hinges on several factors:

- Age: Individuals aged 65 or older are automatically eligible for Medicare, irrespective of their income or health condition. Some exceptions allow certain individuals under 65 to qualify if they have specific disabilities or medical conditions.

- Disability: Those under 65 may qualify if they’ve been receiving Social Security Disability Insurance (SSDI) or certain Railroad Retirement Board (RRB) disability benefits for at least 24 months. Immediate eligibility is granted for individuals with Lou Gehrig’s disease (ALS) upon receiving SSDI or RRB disability benefits.

- End-Stage Renal Disease (ESRD): Individuals of any age with ESRD, requiring dialysis or a kidney transplant, may qualify for Medicare.

It’s important to remember that while Medicare is a federal program, eligibility criteria can vary by state. While Original Medicare (Part A and Part B) is universally available, other parts like Part C (Medicare Advantage) and Part D (Prescription Drug Coverage) have optional enrollment processes.

To ensure seamless coverage, individuals nearing 65, those with disabilities, or those with ESRD should be aware of their eligibility and enroll during the designated periods. The Initial Enrollment Period (IEP), occurring three months before and after the month of eligibility, is crucial.

For personalized guidance on eligibility and enrollment, individuals can reach out to the Social Security Administration (for Original Medicare) or directly to Medicare (for Medicare Advantage and Part D plans).

What are the cost differences?

Costs for private health insurance can differ significantly based on factors like location, age, and the selected coverage type. For instance, plans with higher deductibles typically come with lower monthly premiums compared to those with lower deductibles. This is because insurers offset their expenses by requiring individuals to pay a higher portion of their healthcare costs before the insurance company begins covering treatments.

On the other hand, Medicare plans might entail higher costs since they lack an out-of-pocket limit, a feature mandated for all Medicare Advantage plans.

- Medicare vs. private insurance costs

Comparing the costs of Medicare and private insurance can be complex due to various factors:

- Employers often contribute to private insurance premiums for their employees.

- Some individuals opt for privately administered Medicare Advantage plans, which can offer different cost structures compared to original Medicare.

- The premiums for Medigap policies, which cover expenses like deductibles and copays, vary.

- Medicare premiums typically cover only one person, while private insurers may offer coverage for additional family members.

- Additional factors influencing private insurance costs include age, location, plan benefits, and out-of-pocket expenses.

In general, private insurance tends to be more expensive than Medicare. Many individuals qualify for Medicare Part A with a $0 premium.

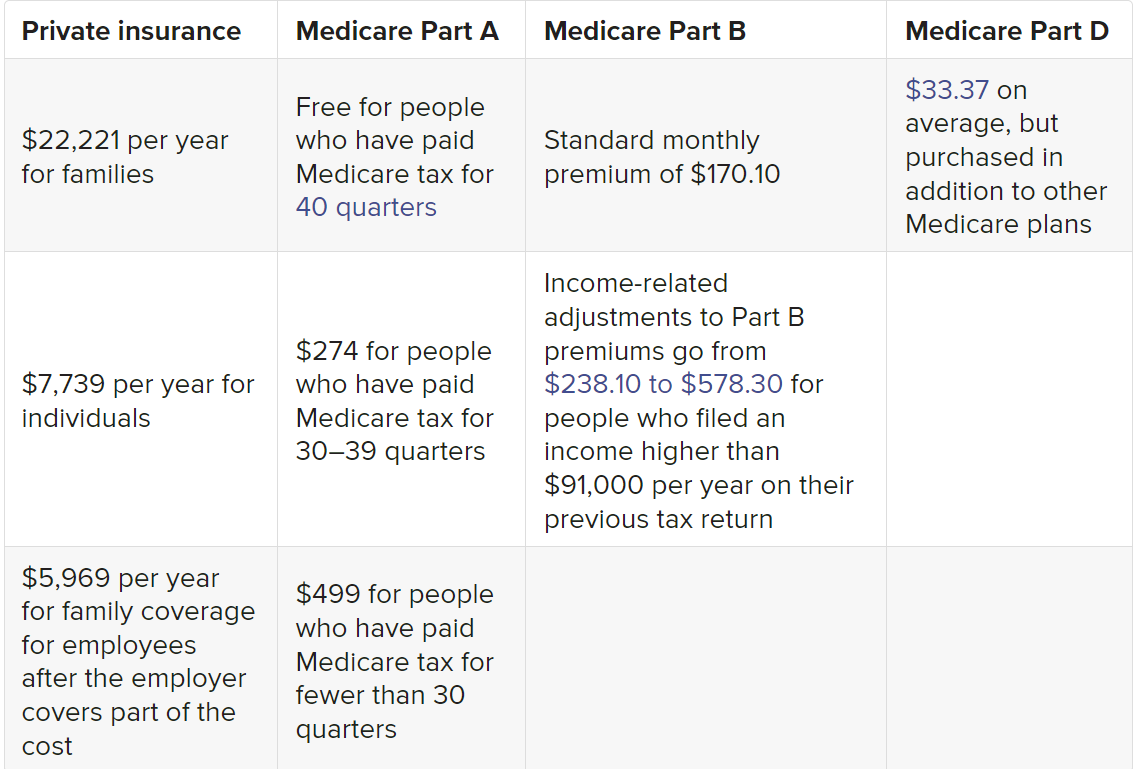

- Medicare vs. private insurance premiums

The table below provides a general comparison of the costs of Medicare and private insurance. However, it shows the average monthly premiums for private insurance in 2021 and the costs for Medicare plans in 2022.

- Medicare vs. private insurance out-of-pocket maximums

When comparing Medicare to private insurance, one key distinction lies in the out-of-pocket maximums. Medicare entails various out-of-pocket costs such as deductibles, coinsurance, monthly premiums, and copays for eligible healthcare services, including prescription drugs. However, private insurance plans typically establish specific regulations regarding out-of-pocket expenses, particularly copays.

For instance, health plans offered by private insurers commonly impose a cap on out-of-pocket costs. This means that once an individual reaches a certain threshold in coinsurance payments, the insurance coverage extends to 100% of the expenses for that benefit until the next membership period. In contrast, Original Medicare lacks an out-of-pocket maximum, leading to potentially unlimited healthcare expenses due to copays for services.

In 2022, the maximum out-of-pocket limit for Advantage plans stood at $8,700 for individuals and $17,400 for families.

- Deductible comparison

Another aspect to consider is the comparison of deductibles between private insurance and Medicare. Deductibles can vary significantly across different plans. Here’s a rough average of deductibles for private insurance plans compared to Medicare Part A and Part B:

- Private insurance: $1,669

- Medicare Part A: $1,556

- Medicare Part B: $233

This indicates that the deductible for Medicare Part A is lower than the average deductible for private insurance plans.

Private health insurance: coverage, options and considerations

4.1. Types of private health insurance plans

Private health insurance plans come in various types, each tailored with distinct features and considerations. Here’s an overview of some common types:

- Health Maintenance Organization (HMO):

- HMO plans establish a network of healthcare providers such as doctors, hospitals, and specialists, which members must utilize to avail coverage.

- Members typically designate a Primary Care Physician (PCP) who oversees their healthcare needs and issues referrals to specialists when required.

- Except for emergencies or certain preventive services, referrals from the PCP are generally necessary to consult specialists.

- HMO plans usually entail lower out-of-pocket expenses for healthcare services compared to other plan types.

- Coverage for healthcare services outside the network may be limited or not provided.

- Preferred Provider Organization (PPO):

- PPO plans also incorporate a network of healthcare providers, but they offer members the flexibility to utilize out-of-network providers at a higher cost.

- Unlike HMOs, PPO plans do not mandate the selection of a primary care physician, and members can directly access specialists without referrals.

- While PPOs provide greater flexibility in choosing healthcare providers, opting for in-network services typically results in lower out-of-pocket costs.

- Coverage for services obtained outside the network is available in PPO plans, albeit with higher coinsurance or copayment requirements.

Exclusive Provider Organization (EPO) plans function similarly to PPO plans but have a distinct limitation: they solely cover in-network care, excluding non-emergency out-of-network services. Members must utilize the designated network of providers for coverage, although they are not obligated to obtain referrals to consult specialists.

Point of Service (POS) plans offer a blend of HMO and PPO characteristics. Members designate a primary care physician who oversees their healthcare and furnishes referrals to specialists within the plan’s network. While members retain the option to seek treatment from out-of-network providers, they incur elevated expenses for such services.

High Deductible Health Plans (HDHPs) feature higher deductibles compared to other plans, necessitating substantial out-of-pocket payments before coverage commences for certain services. Often, HDHPs are coupled with Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs), enabling members to accumulate tax-free funds for medical expenses.

Each private health insurance plan type presents distinct advantages and considerations. Consequently, it’s imperative for individuals to meticulously evaluate plan features, provider networks, and cost-sharing arrangements to identify the most suitable option aligning with their healthcare requirements and financial means.

Comparing Private Health Insurance Coverage and Benefits

When assessing private health insurance options, understanding the coverage and benefits of each plan type is crucial. Here’s a breakdown of coverage and benefits for common private health insurance plans:

Health Maintenance Organization (HMO):

- Coverage: Comprehensive healthcare services including doctor visits, hospital stays, preventive care, and some prescription drugs (with Part D).

- Benefits:

- Lower Out-of-Pocket Costs: Lower deductibles, copayments, and coinsurance.

- Primary Care Physician (PCP): Required, serving as the main healthcare contact and providing specialist referrals within the network.

- Network Restriction: Coverage limited to in-network providers, except for emergencies.

Preferred Provider Organization (PPO):

- Coverage: Broad range of healthcare services similar to HMOs.

- Benefits:

- In-Network and Out-of-Network Coverage: Both options available, with lower costs for in-network providers.

- No PCP Requirement: Members can see specialists without referrals.

Exclusive Provider Organization (EPO):

- Coverage: Comprehensive healthcare services, restricted to in-network providers.

- Benefits:

- In-Network Coverage Only: No coverage for out-of-network services except emergencies.

Point of Service (POS):

- Coverage: Broad range of healthcare services, including both in-network and out-of-network options.

- Benefits:

- PCP Requirement: Needed for specialist referrals within the network.

- Out-of-Network Option: Available, though with higher costs.

High Deductible Health Plan (HDHP):

- Coverage: Comprehensive services with high deductibles.

- Benefits:

- High Deductible: Members pay significant out-of-pocket before coverage kicks in.

- Health Savings Account (HSA) or Health Reimbursement Arrangement (HRA): Tax-free savings for medical expenses.

When comparing private health insurance plans, it’s essential to consider cost-sharing structures, provider networks, coverage specifics, prescription drug coverage, and additional benefits. The choice ultimately depends on individual healthcare needs, budget, and preferences for provider access. Thoroughly reviewing and comparing plan details is recommended before making a decision.

What are the differences in benefits?

Private health insurance and original Medicare plans offer distinct benefits and coverage options.

Both types of plans typically cover hospital care and outpatient medical services, such as doctor’s appointments, physical therapy, and diagnostic tests.

However, private insurers often provide coverage for services not included in Medicare. For instance, Medicare doesn’t cover prescription drugs, necessitating the purchase of a Medicare Part D plan. Conversely, private insurance plans frequently incorporate prescription drug coverage.

Medicare Advantage plans, which substitute original Medicare, may provide coverage more akin to private insurance plans. Many Medicare Advantage plans include dental, vision, and hearing care, as well as prescription drug coverage.

Which is better for those with dependents?

For individuals with dependents, private insurance typically offers a preferable option. Unlike Medicare plans, which cater solely to individuals, private insurers often provide the flexibility to extend health coverage to dependents such as children and spouses. Age also plays a role in the decision between Medicare and private insurance. While Medicare eligibility generally starts at 65 years old or under specific health conditions like end-stage renal disease, private insurance is accessible to individuals of any age.

Can a person have both?

It’s entirely feasible for an individual to possess both Medicare and private insurance concurrently. In such instances, Medicare designates primary and secondary payers. The primary payer settles the claim initially, while the secondary payer covers any remaining expenses not addressed by the primary payer. Medicare determines the primary payer through various regulations; for instance, Medicare assumes the primary payer role when an individual has private insurance through an employer with fewer than 20 employees. To ascertain their primary payer, individuals should directly contact their private insurer.

For some individuals, Medicare could be a more attractive option compared to private insurance, primarily due to cost considerations. Generally, Medicare tends to be more affordable than private insurance plans. However, if an individual’s employer covers their insurance premiums, this can mitigate the financial burden associated with private insurance.

Private insurance might be preferred by individuals with dependents. Unlike Medicare, which only covers the individual, private insurance plans can extend coverage to dependents and other family members under a single policy.

Various factors play into the decision of whether Medicare or private insurance is more suitable for an individual, including their specific medical requirements, geographic location, and desired level of coverage. Ultimately, the choice between the two often boils down to personal preference.