- A real-world landlord insurance example

Let’s examine a practical example of landlord insurance for a rental property. Consider a 3,700 square-foot apartment building comprising three rental units located near downtown Chicago on Fullerton Avenue. The property was purchased for $950,000 in 2018, and the owner estimates its replacement cost to be around $740,000, calculated at $200 per square foot. With all units occupied, the property generates a monthly rental income of $6,000.

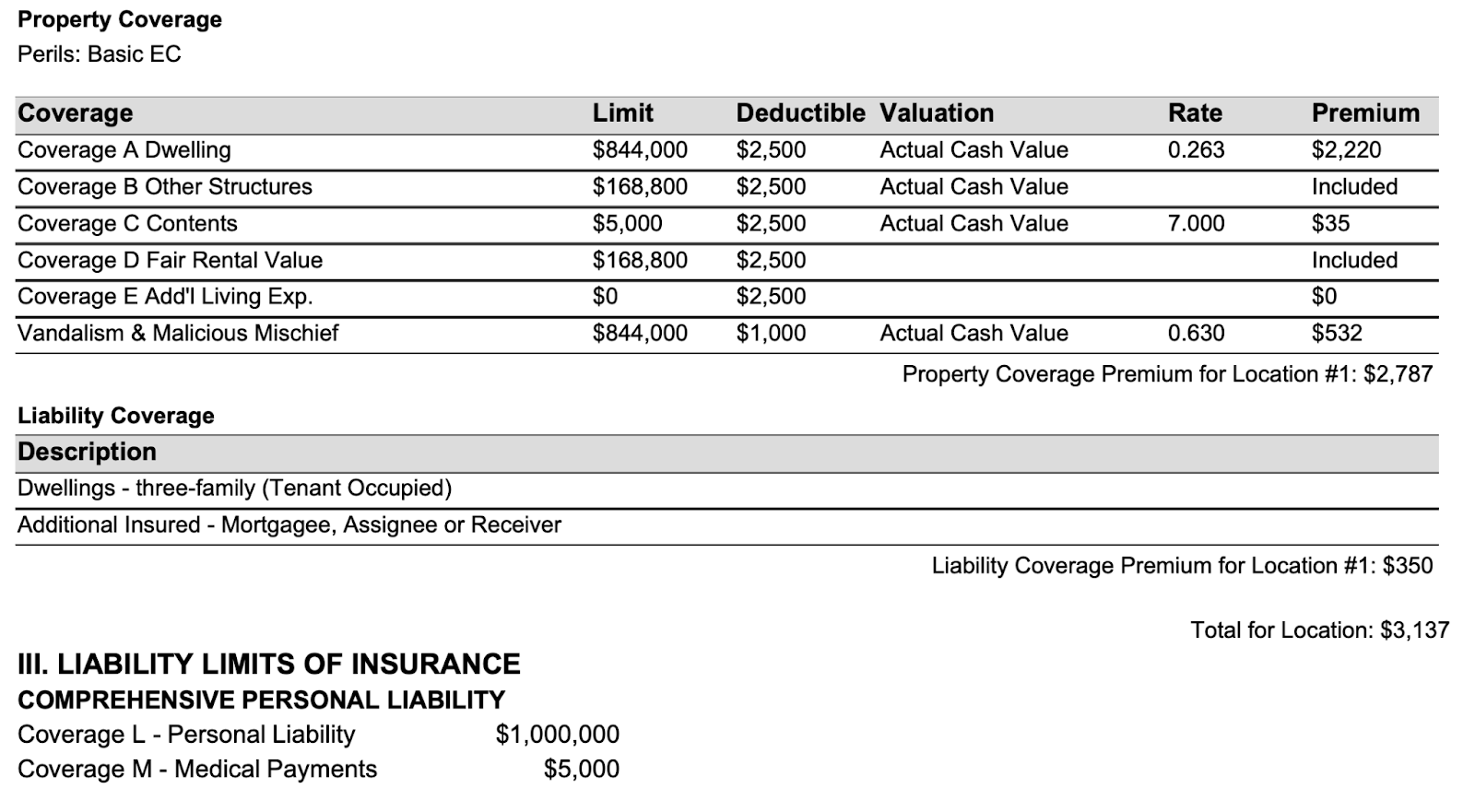

Upon consulting with their insurance agent, the owner obtained three quotes and ultimately opted for a landlord insurance policy from USLI, with an annual premium totaling $3,137. Now, let’s delve into the specifics of the insurance coverage:

- Dwelling: Coverage limit of $844,000 with a $2,500 deductible.

- Other structures: Coverage limit of $168,000.

- Contents (personal property): Coverage limit of $5,000.

- Fair rental value: Coverage limit of $168,800.

- Vandalism: Coverage limit of $844,000.

- Personal liability coverage: Limit of $1,000,000.

- Medical payments: Limit of $5,000.

Examining the cost breakdown reveals discrepancies in premiums:

- Dwelling coverage: Annual premium of $2,200.

- Contents coverage: Annual premium of $35.

- Vandalism coverage: Annual premium of $532.

- Liability coverage: Annual premium of $350.

Dwelling coverage, being the most expensive at $2,200 annually, ensures the ability to rebuild the entire structure in the event of substantial property damage, such as from a fire or natural disaster.

Contents coverage, at a mere $35 per year, protects the landlord’s personal property housed within the rental property, with a limit of $5,000. Notably, this coverage does not extend to the personal property of tenants, which would require a separate renters insurance policy.

Vandalism coverage, costing $532 annually, reflects the heightened risk and expense associated with properties situated in densely populated urban areas.

Lastly, liability coverage, priced at $350 per year, provides $1 million in liability protection along with $5,000 in medical payments for tenants and their guests. Liability considerations significantly contribute to the overall cost of landlord insurance policies.

- What’s wrong with this example

The problem with this scenario is that the owner mistakenly believes that their landlord insurance policy provides comprehensive coverage for any potential damage to their property. However, this assumption is incorrect. Upon closer examination of the policy details, particularly under the “Valuation” column where it states “Actual Cash Value,” it becomes evident that there is a significant gap in coverage.

The term “Actual Cash Value (ACV)” might seem straightforward, implying the actual monetary worth of the property. However, it encompasses the replacement cost minus depreciation. For instance, if the owner installed a roof at a replacement cost of $40,000 in 1999, with $18,000 in accumulated depreciation, the ACV would be reduced to $22,000 ($40,000 – $18,000).

In the event of a covered loss such as damage to the roof, the insurance coverage would only assess the value at $22,000, despite the actual repair cost being $40,000. Compounding the issue, if the owner has a deductible of $2,500, they would only receive a reimbursement of $19,500, leaving them responsible for covering the remaining $20,500 out of pocket.

To mitigate such financial risks, it’s advisable for the owner to seek a new insurance quote with a valuation method based on “Replacement Cost” rather than “Actual Cash Value.” This adjustment not only affects insurance costs but also ensures more comprehensive coverage for the property.

- How Much Does Landlord Insurance Cost in Each State?

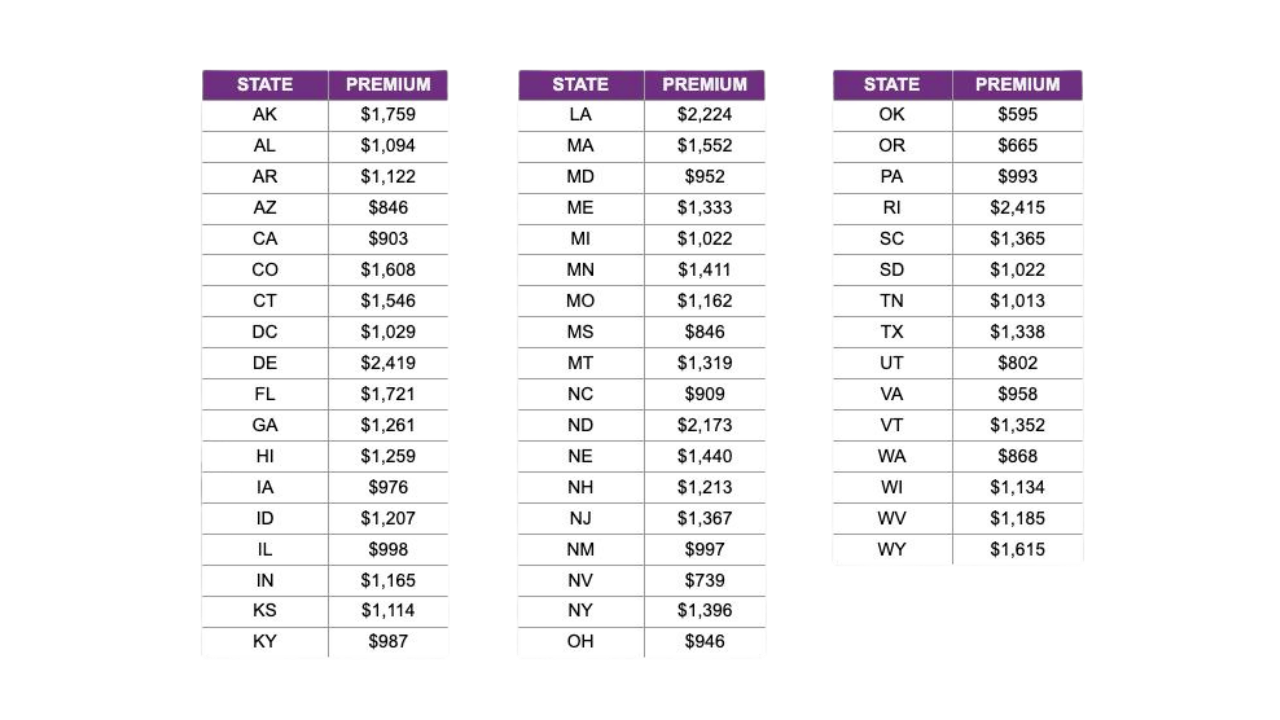

Landlord insurance costs vary significantly across different states due to various factors such as property values, local regulations, and risk assessments. While the national average for landlord insurance stands at approximately $1,478 per year, regional disparities exist.

States with higher property values or increased susceptibility to natural disasters may experience elevated insurance costs compared to the national average. Conversely, areas with lower property values or reduced risk factors might have more affordable insurance premiums.

For a detailed insight into the average landlord insurance costs in each state, individuals can refer to our interactive map or access a state-by-state overview provided below. This information aids landlords in making informed decisions regarding insurance coverage based on their specific location and circumstances.

- Factors That Influence the Cost of Landlord Insurance

Several factors play a role in determining the cost of landlord insurance, with regional disparities being a significant influencer. Insurers assess risk based on various regional factors, including:

- Natural Disasters: States prone to hurricanes, earthquakes, tornadoes, wildfires, or floods face higher risks of property damage, leading to increased insurance premiums to offset potential losses.

- Crime Rates: Areas with elevated crime rates are more susceptible to property damage or theft, resulting in higher insurance costs.

- Property Values: States with higher property values generally incur higher insurance costs due to the increased expense of rebuilding or repairing properties in case of loss.

- Building Age and Condition: Older buildings often have higher insurance costs due to greater wear and tear, which increases the likelihood of maintenance issues.

- Tenant Characteristics: Factors such as the type of tenants and their occupancy behavior can influence insurance rates, with rentals like student accommodations or short-term rentals being deemed higher risk.

- Laws and Regulations: State-specific landlord-tenant laws can impact insurance costs, with states having tenant-friendly laws potentially leading to higher liability risks for landlords and, consequently, higher premiums.

- Claims History: Regions with a history of frequent and severe insurance claims may experience higher premiums due to increased risk.

- Available Coverage Options: Different states may offer varying coverage options and endorsements, which can affect overall insurance costs.

These regional variations result in significant disparities in landlord insurance costs from state to state. Landlords in high-risk areas typically pay higher premiums to safeguard against potential losses, while those in low-risk regions enjoy more affordable rates. Understanding these specific risk factors and collaborating with insurers specializing in regional coverage is essential for landlords. Additionally, comparing quotes from different insurers enables landlords to find the most competitive rates tailored to their location and property type.

- Top Landlord Insurance Providers

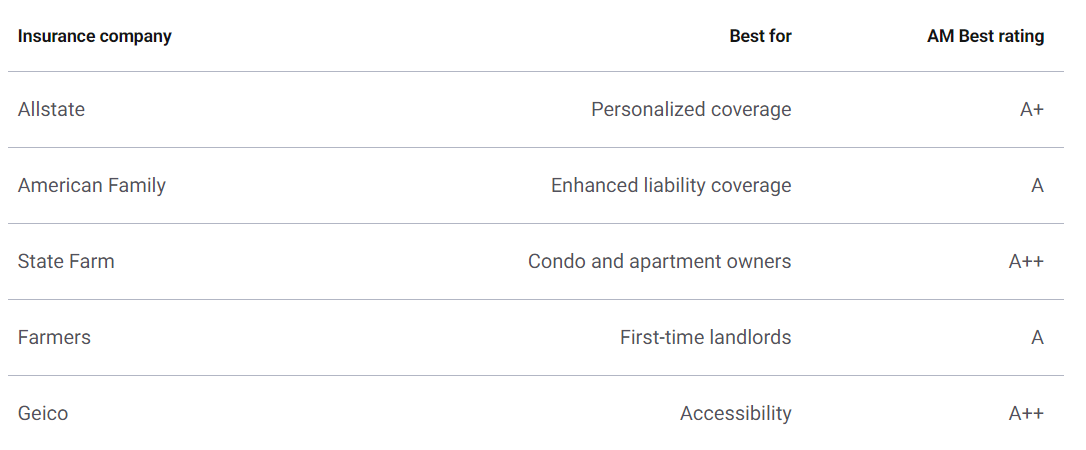

In the search for reliable landlord insurance companies, Bankrate’s insurance editorial team conducted a comprehensive evaluation. This assessment considered various criteria such as financial stability, customer support quality, coverage flexibility, digital resources, and discount opportunities.

As a result of our research, consider initiating your exploration for landlord insurance quotes with these recommended companies:

- Allstate – Personalized coverage

Allstate offers personalized coverage options that may appeal to landlords seeking tailored protection. Their policies include fair income coverage, compensating for lost rental income due to covered events rendering the property uninhabitable. Moreover, Allstate provides various add-ons, such as vandalism coverage for vacant units, building code coverage, and insurance for rental properties under construction. However, prospective customers should note that Allstate does not facilitate online quoting for landlord insurance; instead, they need to reach out to the company or a local agent for a quote.

- American Family – Enhanced liability coverage

American Family caters to landlords looking for comprehensive coverage, including commercial umbrella liability protection. Additionally, they offer policies tailored for business owners renting out properties, covering essential business aspects not typically included in standard landlord policies, like auxiliary structure coverage. New landlords may find value in AmFam’s Landlord Toolbox, featuring resources on topics such as state tenant laws, property maintenance, and tenant selection. However, it’s worth noting that American Family has limited availability across states and does not provide an online quoting option for landlord insurance.

- State Farm – Condo and apartment owners

State Farm provides specialized landlord insurance policies tailored to different property types, including homes, condos, and apartments. These policies encompass essential features like loss of rents coverage. Apartment landlord policies include additional benefits such as equipment breakdown coverage and reimbursement for heating and air conditioning losses. State Farm also offers potential discounts for home safety devices and boasts a network of local agents for personalized service, which can be beneficial for those navigating the landlord insurance market.

- Farmers – First-time landlords

Farmers offers relatively straightforward landlord insurance policies with options for endorsements like loss of rents coverage, personal property coverage, and coverage for other structures. Their SmartMove screening tool aids landlords, particularly first-timers, in selecting suitable tenants by providing comprehensive tenant reports to mitigate risks. Like many competitors, Farmers does not offer online quotes for landlord insurance policies.

- Geico – Accessibility

Geico stands out for landlords seeking robust coverage alongside convenient digital property management tools. Their website and mobile app facilitate easy policy management and claims filing. Geico’s coverage options include loss of rent payments coverage and various add-ons such as vandalism coverage and additional building code construction expenses coverage. Notably, Geico offers online quoting for landlord insurance, although policies are underwritten by affiliate companies, leading to potential variations in underwriting.

- How to find the best cheap landlord insurance

Finding the most affordable landlord insurance that suits your needs involves considering various factors such as property type, location, budget, and personal preferences. For instance, landlords managing multiple properties might prefer insurers offering user-friendly mobile apps for convenient policy management. Those with older rental properties may seek insurers providing building code coverage to safeguard their property during renovations. Here are steps to help you find the best cheap coverage:

- Compare coverage options: Different insurers offer various coverage types and endorsements. Assessing your coverage requirements and comparing options from multiple carriers can help you identify the most suitable ones.

- Consider third-party ratings: Organizations like AM Best, J.D. Power, and the National Association of Insurance Commissioners (NAIC) evaluate insurers based on financial stability, customer satisfaction, and digital tools. Reviewing these ratings can give insights into an insurer’s ability to meet your needs.

- Compare quotes and discounts: Your insurance costs depend on factors such as property characteristics, personal rating factors, and coverage selections. Obtaining quotes from different insurers enables you to find the most cost-effective option. Additionally, exploring potential discounts offered by each insurer can further reduce your premiums.

- Seek guidance from a licensed insurance agent: Consulting with an insurance agent can provide valuable assistance throughout the landlord insurance shopping process, helping you make informed decisions tailored to your specific requirements.

- FAQs:

How can I obtain a quote for landlord insurance?

You can usually obtain quotes for home and auto insurance online, but most insurers still require you to contact an agent for a landlord insurance quote. When you reach out to an agent, they will request details about your property, such as its location, size, and features, along with personal information like your age and claims history. In many states, your credit history and marital status can also influence your rate.

Is landlord insurance different from homeowners insurance?

Yes, it is. One significant difference is that landlord insurance does not cover the personal belongings of the tenant. While a homeowners insurance policy includes coverage for your belongings, a landlord policy only covers the structure of the building and other property structures. To ensure coverage for their personal belongings and loss of use, renters need to purchase their own renters insurance policy. Landlord insurance typically also provides coverage types not found in a personal homeowners insurance policy, such as loss of rent coverage to supplement lost income if the structure becomes uninhabitable due to a covered loss.

Is landlord insurance mandatory?

Landlord insurance is not legally required anywhere in the U.S. However, your mortgage lender will likely require you to have an insurance policy on your rental property as a condition of the loan. Most insurance experts recommend having landlord insurance, even without a mortgage, to protect against having to pay out-of-pocket if your property is damaged or destroyed in a fire, storm, or other named peril.

Can landlords insist on tenants having renters insurance?

Although renters insurance is not legally mandatory, landlords can require tenants to have a policy in place as a condition of the lease. The requirement for renters insurance is typically outlined in the rental contract.

Is landlord insurance costly?

The cost of a landlord insurance policy can vary significantly based on the property’s characteristics, location, and the landlord’s personal factors. Landlord insurance typically does not include coverage for personal property, which may make it cheaper than homeowners insurance. However, insurers may view rental properties as riskier to insure than owner-occupied homes, as tenants may be less likely to maintain the properties regularly. The most effective way to determine potential costs for landlord insurance is to compare quotes from multiple providers.